CFOs today are under growing pressure to deliver measurable business outcomes from every outsourced Finance and Accounting (F&A) engagement. Yet, many F&A services outsourcing arrangements still rely on Full-Time Equivalent (FTE)-based pricing models that measure success by inputs—i.e., people, hours, and effort.

The result? Misaligned incentives, stagnant processes, and rising operational costs.

Forward-looking organizations are breaking this cycle by adopting an outcome-based model that links provider fees to measurable business results such as lower Days Sales Outstanding (DSO), reduced cost per transaction, faster close cycles, or improved accuracy rates.

According to the ISG Provider Lens Global F&A Services Outsourcing Report (2024), traditional FTE pricing is being steadily replaced, with leading service providers now linking 70-100 percent of the contract value to business outcomes.

This shift reflects a growing demand for accountability, shared value creation, and nimbleness in adapting to and staying ahead of changing business priorities.

Why Traditional FTE-Based Models Fall Short

While FTE-based models offer predictability, they limit strategic and operational value, particularly for organizations pursuing digital transformation and continuous improvement.

Key challenges include:

- Input-focused performance: FTE models measure effort (headcount, hours) rather than tangible business outcomes, such as faster close or improved accuracy.

- Misaligned business objectives: Enterprises prioritize financial outcomes (e.g., lower DSO, improved cash flow), while providers under FTE models aim to maintain staffing levels and revenue.

- Rising cost-to-serve: As digital transformation scales, maintaining large FTE teams inflates costs without improving results.

- Limited performance visibility: Without outcome-based KPIs, enterprises struggle to link service delivery to business impact.

- Transactional engagement model: Without shared accountability for results, F&A outsourcing partnerships remain operational rather than value-driven.

Outcome-Based Pricing vs Traditional Pricing Models

The shift toward outcome-based pricing becomes clearer when compared directly with traditional engagement models that dominate finance and accounting services.

FTE-Based Model (Input-Driven):

Pricing is tied to headcount and effort. While it offers cost predictability, it does not incentivize efficiency or innovation. Providers are rewarded for maintaining resources rather than improving outcomes.

Fixed Pricing Model:

A predefined cost is set for a defined scope. This model works well for stable, repetitive processes but lacks flexibility when volumes fluctuate or when continuous improvement is required.

Hourly Billing Model:

Charges are based on time spent. While simple, it often leads to inefficiencies, as increased effort directly translates into higher costs without guaranteeing better results.

Subscription-Based Model:

A recurring fee for bundled services. It offers predictability and ease of budgeting but typically lacks direct alignment with performance or business impact.

Outcome-Based Pricing Model (Value-Driven):

In contrast, outcome-based pricing links fees to measurable results—such as reduced DSO, lower cost per invoice, or faster close cycles. This model aligns provider incentives with enterprise goals, ensuring that both parties are accountable for performance, efficiency, and continuous improvement.

The fundamental difference lies in what is being paid for:

Traditional models reward effort, while outcome-based models reward results.

Want to see how these outcomes translate in real business scenarios? Explore 7 success stories of companies that transformed their financial operations through outsourced accounting services.

What the Shift Toward Outcome-Based Models Means

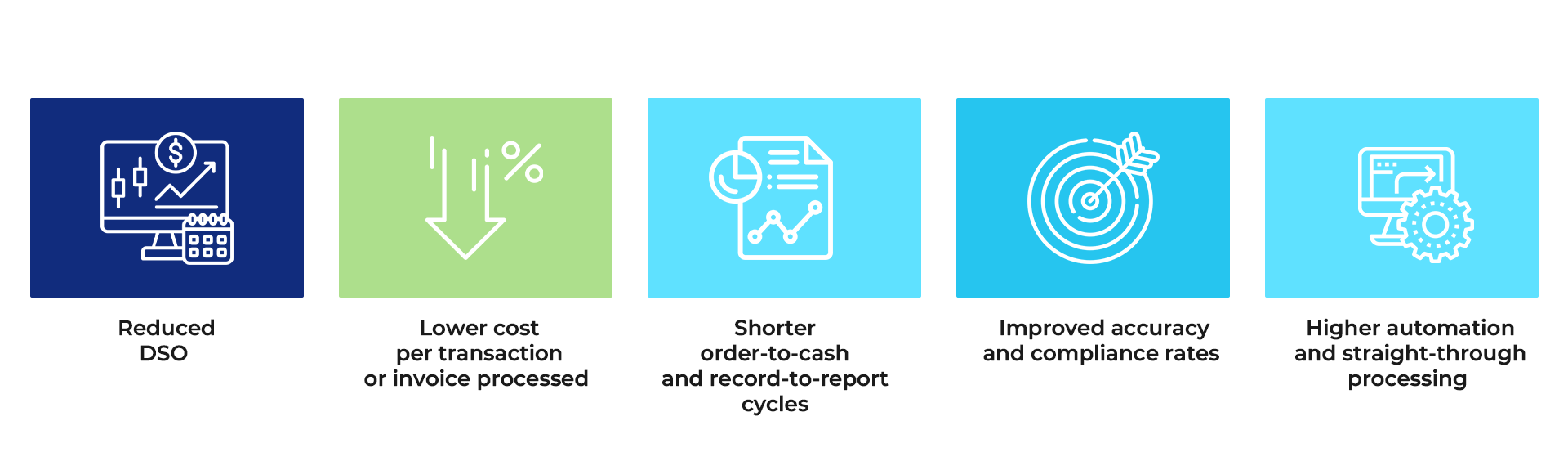

For CFOs seeking new-age F&A solutions and more value from their outsourced F&A services, the outcome-based model enables them to turn F&A into a performance engine rather than a back-office function. These engagements ensure that external partners share accountability for tangible improvements tied to defined performance metrics, such as:

By aligning incentives around results rather than effort, outcome-based models strengthen performance visibility, enhance agility, and embed continuous improvement into daily operations.

How Outcome-Based Pricing Works in Finance and Accounting Services

An outcome-based pricing model operates by structurally aligning financial incentives with measurable business performance. Instead of paying for activities, organizations pay for results that directly impact financial health.

The model typically follows a structured approach:

1. Define Business Outcomes

Organizations identify high-impact financial metrics such as:

- Days Sales Outstanding (DSO)

- Cost per transaction

- Invoice processing cycle time

- Accuracy and error rates

These outcomes are selected based on their relevance to working capital, cost optimization, and operational efficiency.

2. Establish Baselines and Targets

Historical performance data is used to set a baseline. From there, realistic and measurable improvement targets are defined—for example, reducing DSO by a specific percentage or lowering invoice processing costs.

3. Link Pricing to Performance

A portion (or majority) of the service provider’s fees is tied to achieving these predefined outcomes. This may include:

- Incentives for exceeding targets

- Penalties or reduced fees for underperformance

4. Enable Real-Time Performance Tracking

Advanced analytics and dashboards are used to monitor KPIs continuously. This ensures transparency and allows both the enterprise and provider to track progress against agreed benchmarks.

5. Continuous Optimization Through Governance

Regular governance reviews help identify bottlenecks, refine processes, and recalibrate targets as business needs evolve. This ensures the model remains dynamic rather than static.

By embedding accountability into the pricing structure, outcome-based models transform F&A outsourcing into a performance-led partnership rather than a transactional service.

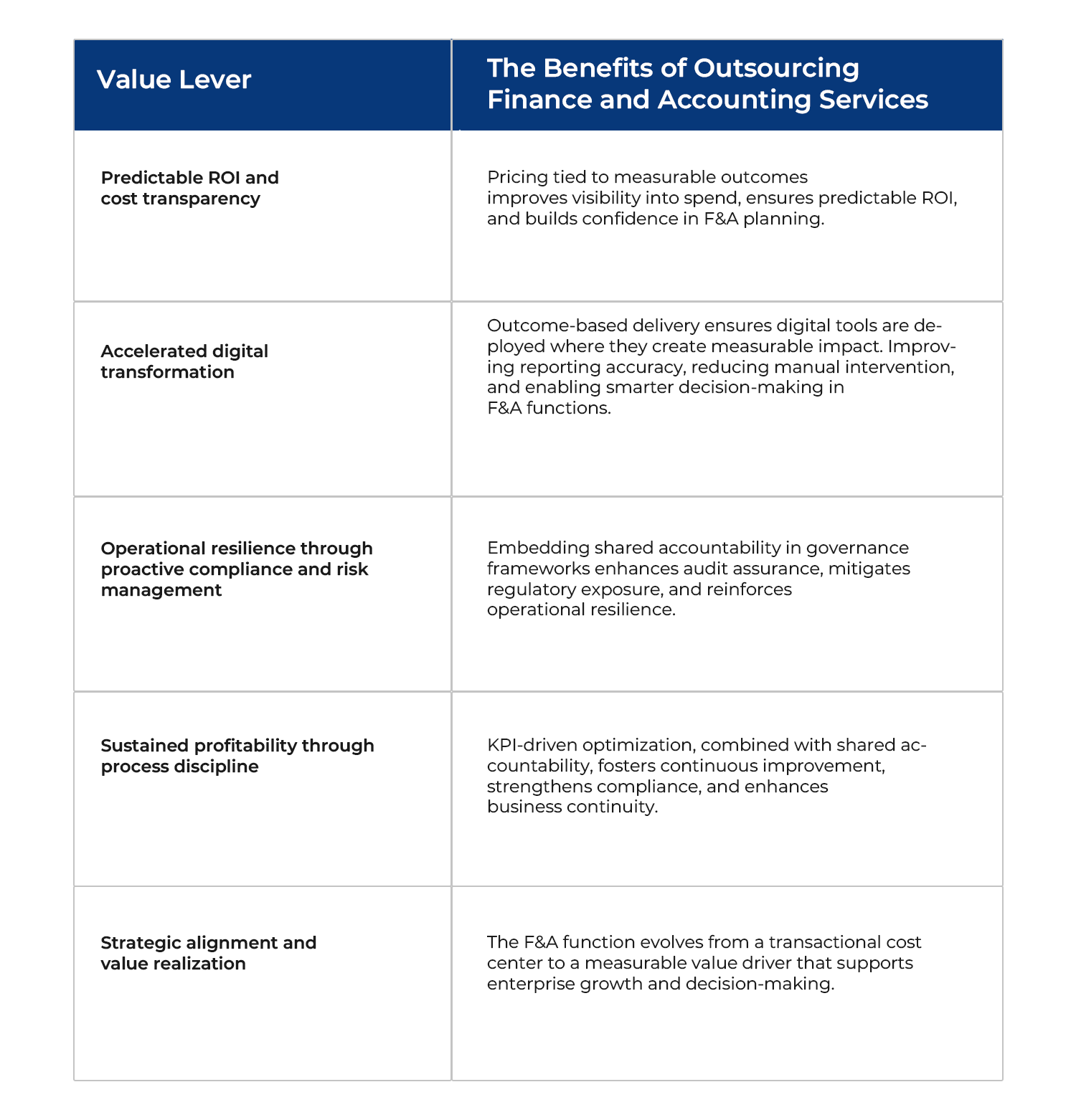

How Outcome-Based Models Create Value for Enterprises

For finance leaders, outcome-based delivery redefines outsourced F&A services from cost management to a measurable performance partnership. It positions F&A operations to support enterprise goals, such as working capital efficiency, digital transformation, and change readiness.

Key Benefits of Outcome-Based Pricing in Finance and Accounting Services

Outcome-based pricing repositions finance and accounting from a cost center to a value-generating function. Aligning incentives with measurable performance, outsourced finance and accounting services delivers both operational and strategic advantages.

1. Direct Alignment with Business Outcomes

Service providers are incentivized to improve metrics that matter—cash flow, cost efficiency, and financial accuracy—ensuring that delivery directly contributes to enterprise goals.

2. Improved Working Capital Efficiency

Metrics such as DSO and cycle times are actively optimized, leading to stronger liquidity and better cash flow management.

3. Built-In Continuous Improvement

Unlike static pricing models, outcome-based structures encourage ongoing optimization through automation, process redesign, and analytics.

4. Greater Cost Transparency and Control

Organizations gain clearer visibility into what they are paying for—measurable results rather than effort—making ROI easier to track and justify.

5. Stronger Accountability and Partnership

Both the enterprise and service provider share responsibility for outcomes, creating a more collaborative and performance-driven engagement model.

6. Acceleration of Digital Transformation

Providers are motivated to deploy automation, AI, and analytics tools to meet performance targets efficiently, speeding up transformation initiatives.

Building the Foundation for a Successful Outcome-Based Model

Transitioning from an FTE-based structure to an outcome-based model requires more than a strategy shift. It demands a new governance mindset, data discipline, and shared performance accountability. CFOs should focus on five critical enablers:

1. Prioritize Enterprise-Level Outcomes Over Operational Metrics

Begin with outcomes that directly impact financial performance, such as working capital efficiency, acceleration of the cash conversion cycle, or reduction in the cost per transaction. Avoid focusing only on local efficiency metrics. Anchor success to measurable enterprise KPIs that impact the bottom line by setting clear baselines and target improvements.

2. Build a KPI Architecture that Connects Operations to Strategic Value

Develop a structured KPI hierarchy where process metrics, such as cycle time and accuracy, link to efficiency indicators, such as cost per transaction and error rates, which in turn connect to strategic goals like liquidity and EBITDA impact. This alignment ensures CFOs have a clear line of sight from execution to enterprise value creation.

3. Establish Transparent, Joint Governance with Real-Time Oversight

Establish formal governance structures that facilitate agile, data-driven review sessions between the enterprise and the service provider. Both parties should monitor progress against agreed outcomes, respond quickly to deviations, and co-develop improvement plans.

4. Balance Risk and Reward to Sustain Innovation and Viability

Contracts should clearly allocate financial responsibility, striking a balance between incentives for providers to exceed outcome targets and accountability for underperformance. Establishing transparent incentive mechanisms and accountability measures helps sustain innovation and strengthens the F&A partnership.

5. Continuous Outcome Optimization

Embed advanced analytics that provide real-time insights into performance, bottlenecks, and risk areas. This approach enables enterprises to move beyond mere SLA compliance, facilitating iterative operational refinement, improved financial predictability, and implementation of agile processes in complex regulatory environments.

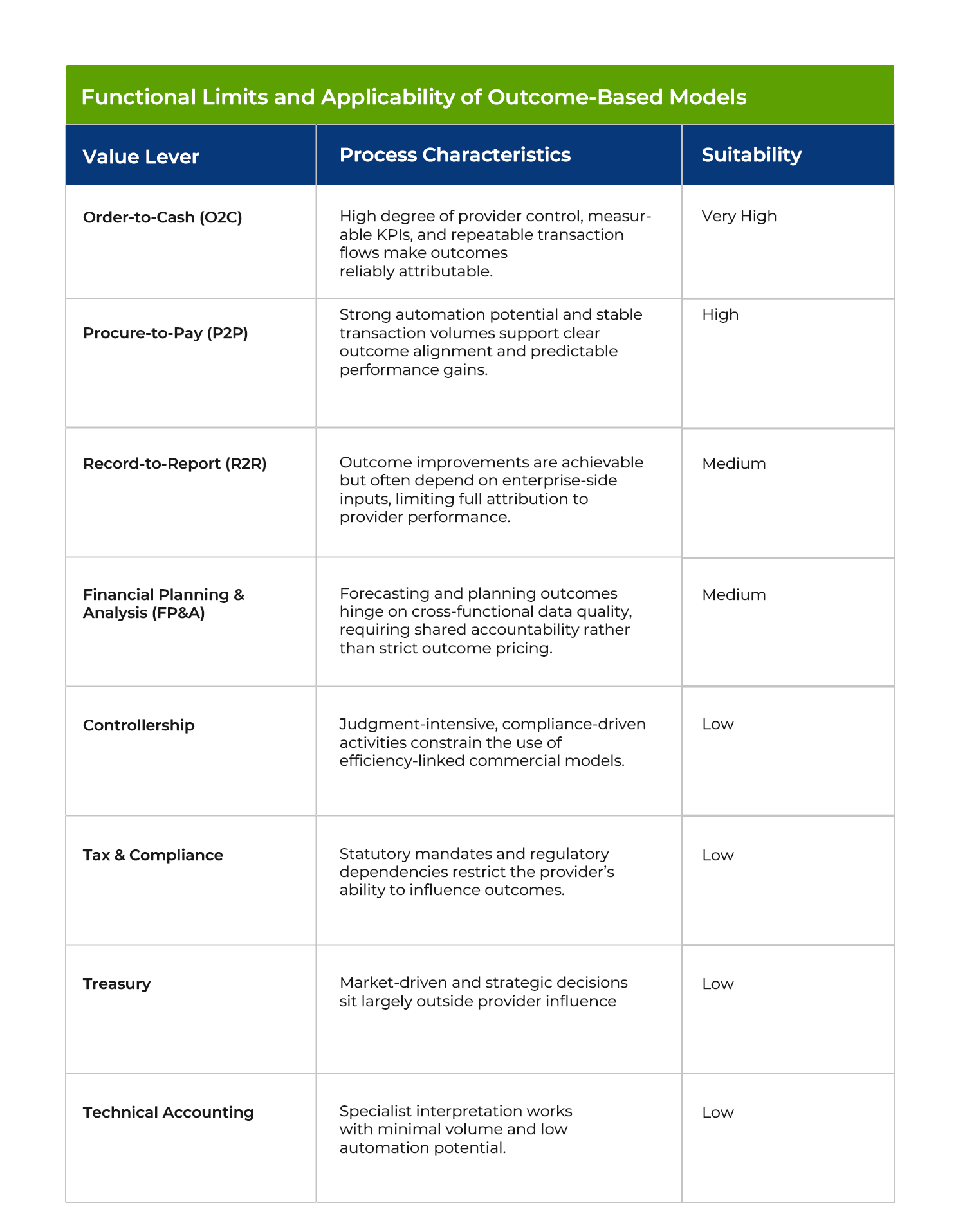

What CFOs Must Consider Before Making the Shift

An outcome-based model delivers value in high-volume, controllable processes. However, its applicability is not universal across the F&A landscape. CFOs evaluating this model should consider several operational constraints that influence feasibility and effectiveness.

1. Outcome Controllability Varies Across Finance Functions

Not all finance processes operate within the provider’s span of control. Outcomes in areas such as treasury, technical accounting, or forecasting depend on enterprise-side policies, business inputs, and external market factors. When providers have limited influence on the drivers of performance, attaching commercial value to outcomes can create misaligned incentives and unclear accountability.

2. Judgment-Driven Activities Resist Standardized Outcome KPIs

Functions such as controllership, tax, statutory reporting, and technical accounting rely primarily on professional judgment and policy interpretation rather than transactional throughput. Attempts to engineer outcome KPIs in these areas often lack precision and risk, oversimplifying work that is inherently qualitative and compliance-led.

3. Regulatory and Audit Dependencies Require Precision Over Speed

Compliance-heavy functions must adhere to strict statutory requirements, accounting standards, and audit expectations. In these domains, the consequences of errors outweigh the benefits of speed or productivity gains. Outcome-based models that emphasize cycle-time or volume improvements may inadvertently shift focus away from accuracy, increasing compliance risk.

4. Low-Volume or Episodic Processes Limit Measurable Outcome Attribution

Outcome-based models rely on stable transaction volumes and repeatability to generate statistically meaningful improvements. Treasury operations, technical accounting, M&A support, and certain controllership activities are low-volume or event-driven, making it difficult to establish reliable baselines or attribute outcomes directly to provider performance.

The Way Forward

The move to outcome-based delivery marks a pivotal shift in how outsourcing F&A services generates business value. In essence, this shift reflects growing demand for measurable impact and risk-sharing between clients and partners, with success being defined by continuous improvement rather than volume-based delivery. Enterprises that adopt outcome-based delivery models today will be better equipped to anticipate and respond to change, turning F&A functions into a strategic growth enabler rather than a cost center.

At Accounting To Taxes (ATT), we help finance leaders move beyond effort-based outsourcing to achieve real outcomes and resilient growth. Our ADIS Framework operationalizes this shift by aligning analytics, digital tools, insights, and service workflows to deliver measurable improvements across the F&A value chain.

Ready to transform your F&A function?

Explore how our domain expertise and proprietary framework can help you build a connected, intelligence-driven operation that accelerates decision-making at scale.